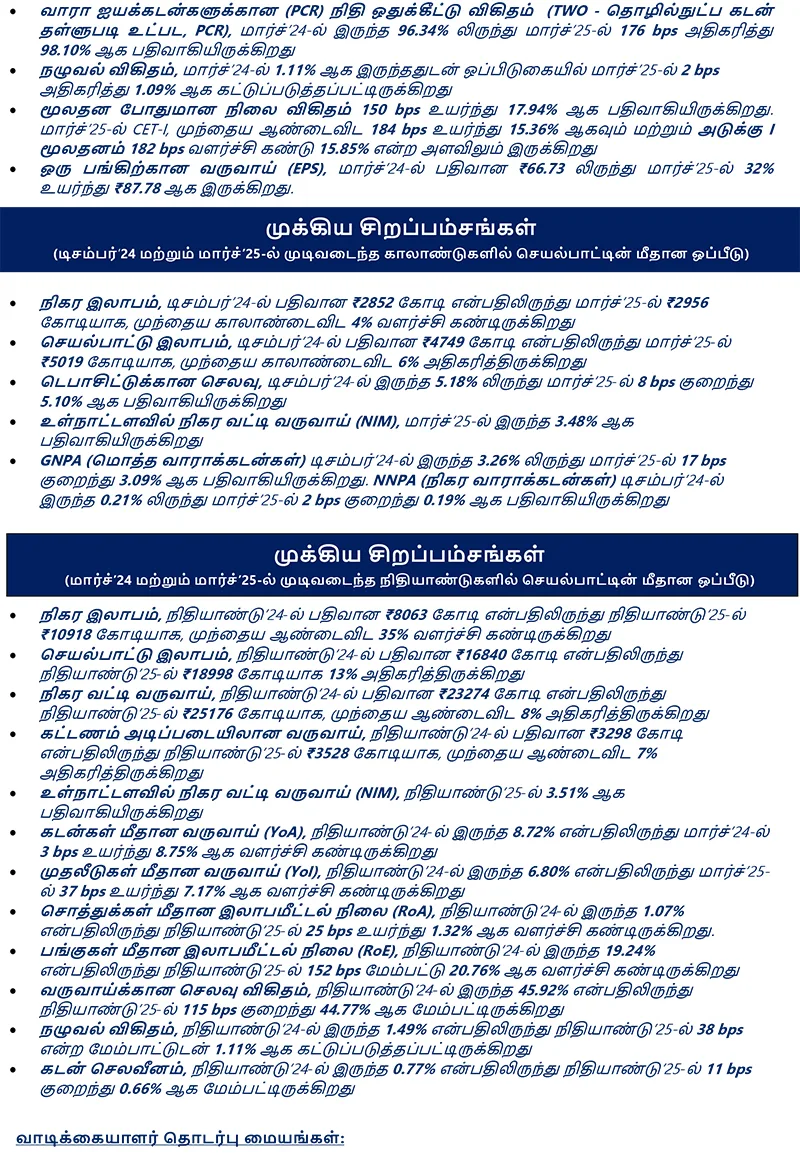

Indian Bank Q4 net profit jumps 32% to Rs 2,956 crore

During the quarter, the bank’s total income increased to ₹18,599 crore from ₹16,887 crore a year ago

Public sector lender Indian Bank has reported an annual profit exceeding ₹10,000 crore for the first time in FY25, marking a 35 per cent year-on-year growth. For the March 2025 quarter, the bank’s net profit rose by around 32 per cent .

The Board has recommended a dividend of ₹16.25 per equity share, equivalent to 162.50 per cent of the paid-up equity capital, for the financial year 2024–25. It has also approved fund-raising plans amounting to ₹12,000 crore, including: ₹5,000 crore of equity capital via QIP, FPO, rights issue, or a combination thereof; ₹2,000 crore through the issuance of Basel III-compliant AT-1 perpetual bonds or Tier-2 bonds in one or more tranches; and ₹5,000 crore via infrastructure bonds.

Indian Bank reported a net profit of ₹10,918 crore in FY25 compared with ₹8,063 crore in FY24. In Q4 of FY25, the Chennai-headquartered bank’s net profit rose to ₹2,956 crore from ₹2,247 crore in the year-ago quarter.

“Indian Bank has delivered a good set of numbers in both Q4 and the full year ending FY25, marked by robust profitability, improved asset quality and solid business momentum with good tractions in the RAM (retail, agriculture & MSME) sector. For the first time, the bank has crossed ₹13 lakh crore in total business. Also, for the first time, its Profit After Tax (PAT) has exceeded ₹10,000 crore in a year, said Binod Kumar, Managing Director & CEO of Indian Bank.

He added that a noteworthy achievement was the reduction in SMA (Special Mention Accounts), which indicate stress in the loan book. The SMA ratio, which stood at 15.59 per cent at the end of FY24, declined to 8.06 per cent by the end of FY25—nearly halving over the year.

Provisions (excluding taxes) fell to ₹795 crore in Q4 FY25, down from ₹1,248 crore in the year-ago quarter. Fresh slippages were at ₹1,393 crore versus ₹1,238 crore last year. Recovery of bad debt stood at ₹2,548 crore, reflecting a growth of 25.6 per cent .

Deposits grew by 7 per cent , bringing total deposits to ₹7.37 lakh crore. Advances rose by 10 per cent to ₹5.88 lakh crore. The bank maintained a CASA (Current Account Savings Account) ratio of 40 per cent .

The Credit-Deposit (CD) ratio stood at a healthy 79.79 per cent . Its RAM (Retail, Agriculture, MSME) portfolio crossed ₹3.5 lakh crore, reflecting 13 per cent year-on-year growth: retail grew 14 per cent , agriculture 14 per cent , and MSME 12 per cent .

Asset quality continued to improve. Gross NPA stood at 3.09 per cent as of March 31, 2025, down from 3.95 per cent a year earlier, while net NPA fell to 0.19 per cent from 0.43 per cent . The Provision Coverage Ratio (PCR) stood at 98.10 per cent . “Even without technical write-offs, we have managed to reduce both gross and net NPAs,” Kumar said.

The cost of deposits decreased by 8 basis points to 5.10 per cent for the March 2025 quarter but increased by 24 basis points year-on-year from 5.01 per cent . Due to two repo rate cuts, the yield on advances rose by 28 basis points during the quarter and by 3 basis points year-on-year.

{kind=link}